A regular term insurance policy offers crucial money safety. It pays your family a lump sum if you pass away. This basic plan ensures your loved ones get funds. This money helps them manage future costs and keep their lifestyle.

However, a basic term plan has its limits. It typically covers only death. It might not give money for other life events. These events could be an accidental disability or finding out you have a serious illness. Such times can cause you to lose income and face high medical bills.

Term insurance riders are extra choices. They make your main policy's protection stronger. Riders help fill these coverage gaps. Knowing about these improvements is key for full financial planning. This guide will tell you about rider life insurance types, their benefits, and how to pick the right additions for what you need.

What are term insurance riders and how do they work?:

What is a rider in a term insurance policy? A term insurance rider is an extra choice you can add. It makes your regular term life insurance policy stronger.

These term insurance riders are not separate policies. Instead, they join your main term plan for a small extra cost. Think of it like picking optional upgrades when you buy a new car. You make your car just right for you. Similarly, a rider life insurance plan helps you change your policy. It lets you meet your exact needs.

What does a rider in insurance term mean? It offers more money protection. How do life insurance riders work? They give you added coverage for specific events, not just death. These term insurance riders benefits often protect you if you get a serious illness or an accidental disability. Common term insurance riders types include Accidental Death or a Terminal Illness Benefit. You typically choose a rider when you first buy your main policy. Most insurers do not let you add them later.

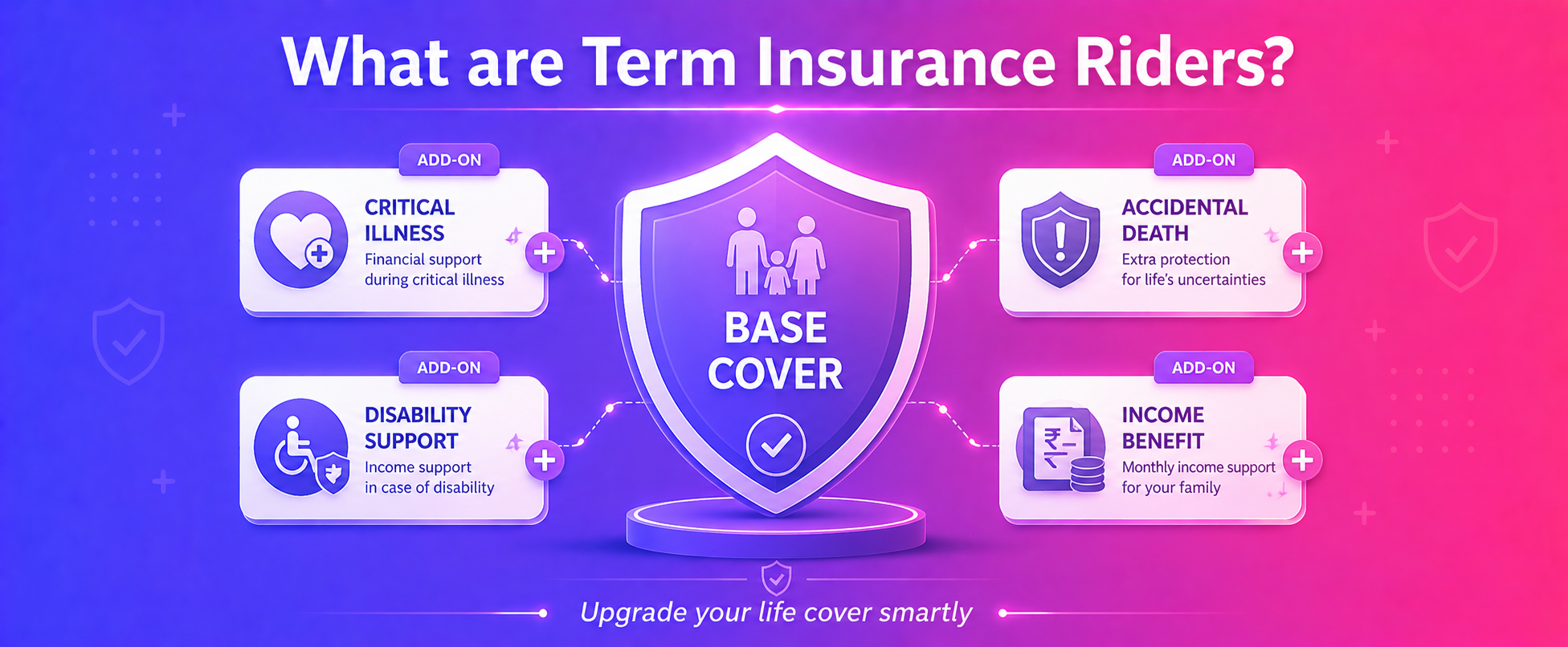

Types of term insurance riders

You can add extra features to your basic term policy. These features help cover different life risks. What you can add often depends on your chosen insurance company. So, what are the different types of riders in term insurance? Let's explore a few common ones. Choosing a rider life insurance option gives you more coverage for a small extra premium amount.

Here are some common term insurance riders:

1. Critical illness rider

A critical illness rider gives you one payment. You get this money if a doctor confirms you have a serious illness listed in your plan. This payment helps with large medical bills or lost income. For example, think about a 1 crore term plan. If you add a 20 lakh critical illness rider, you get 20 lakh when diagnosed. This rider money does not lower your main life coverage amount.

- It helps protect against specific serious illnesses like cancer or a heart attack.

- You get a single payment when a doctor confirms the illness.

- The money paid out does not change your main policy's death benefit.

- This money helps lessen financial worries and treatment costs.

Best For: People who want financial safety during major health problems.

2. Accidental death benefit rider

An accidental death benefit rider is a type of rider life insurance. It gives extra money with your life insurance. Your family gets this money if the person covered dies from an accident. This payment adds to your main life insurance amount. For example, imagine a life plan for 1 crore. It also has a 50 lakh accidental death rider. If death is due to an accident, the person you choose usually gets 1.5 crore.

- It offers more money for an accidental death.

- This makes your family's money situation stronger.

- The payout is separate from your basic life insurance.

- This rider life insurance option gives special protection against sudden accidents.

Best for: People who want more money help for their family after an accidental death.

3. Accidental total and permanent disability rider

This rider gives important money help. It pays you if an accident causes a total and permanent disability. This means you cannot work. The money can be one large payment or regular payments. It replaces the pay you lose. Many plans also stop future payments for your main policy. This rider life insurance gives strong money protection.

- You get money for lost pay after an accident.

- It helps when you cannot earn money because of an injury.

- It stops future payments for your main policy.

- This gives more help to policyholders during a hard time.

Best For: People who want to protect their income after an accidental injury.

4. Waiver of premium rider

A Waiver of Premium Rider stops payments for your term plan. This happens if the insured person gets a critical illness or becomes permanently disabled. It helps your rider life insurance policy stay active. This is true even if you cannot earn money or make payments. This gives important Policyholder Benefits.

- It stops your future premiums if you become disabled or seriously ill.

- The main life insurance plan remains fully active.

- You will not need to make any more payments.

- This offers financial help when you face tough times.

Best For: This rider is good for people who want to protect their policy. It helps those worried about losing income from a critical illness or disability.

5. Income Benefit Rider

Instead of a lump sum payout, this rider provides regular monthly income to your family after your death.

Why you should consider it:

- Helps manage day-to-day expenses

- Acts like a salary replacement for your family

Best for: Families dependent on a single income source

6. Terminal Illness Rider

If you are diagnosed with a terminal illness (with limited life expectancy), this rider pays out a portion of the sum assured in advance.

Why you should consider it:

- Helps cover end-of-life medical expenses

- Provides financial support during critical times

What are the key benefits of adding riders to a term policy?

Adding riders to a term policy makes your financial protection much stronger. This clearly answers the question, "What are the benefits of a rider in insurance?" Why should you buy term insurance riders? They build a more robust safety net for your family.

- Extra Protection: Riders offer more coverage than just the basic death payment from your term plan. They shield you from specific risks. These often include accidents or serious illnesses. For example, an Accidental Death Benefit Rider or a Critical Illness Rider helps. This added safety can support you during tough times.

- Good Value for Money It is typically cheaper to add riders than to buy separate insurance policies for each risk. This makes them a smart choice for your money plans. Are insurance riders worth it? Their lower cost often makes them a good investment.

- You can change your rider life insurance policy to fit your exact needs. This flexibility lets you build a plan that truly matches what your family needs as life changes.

- Tax Benefits: Some riders, like a Critical Illness Rider, may offer tax benefits under current Indian tax laws. The money you pay for these riders can count for tax deductions under Section 80D of the Income Tax Act, 1961.

How to choose the right term insurance riders for your needs

Choosing the right rider life insurance protects your family's money. This guide helps you learn How to select the right insurance riders? It also shows What to consider when choosing insurance riders? Good choices depend on your personal needs. No single answer works for everyone. This helpful guide will help you decide Which riders should I add to my term plan?

Assess your health, family history, and lifestyle risks:

Your health facts and your family's health history are very important. They help you choose rider life insurance. These facts also help decide if you need more coverage for certain health problems. Your daily life and job change your best choices too.

- Think about your family's history of serious diseases, like cancer.

- Do you have any current health problems that need protection?

- Consider if your job has dangers or a lot of travel.

- Look at your daily life for possible health dangers.

Best For: People who want to change their policy based on their health, family background, and job risks.

Evaluate your financial dependents and liabilities

Many people depend on your income. Your financial debts also matter greatly. These points directly shape your choice of rider life insurance. For sole earners, a Waiver of Premium rider becomes key. This rider helps keep the policy active if the main earner cannot work due to a disability.

- Think about who relies on your income for daily needs.

- Consider any debts your family might need to cover.

- Do you have a home loan or other big financial duties?

- How would your family manage without your monthly earnings?

Balance the additional cost against potential coverage

Adding any rider life insurance option increases your policy's yearly price. It's smart to plan for these added costs well. First, find the full yearly price with all the extra covers you wish to get. This helps keep your financial plan affordable for many years. Always pick riders that cover your biggest and most likely risks first. Don't add every choice without careful thought.

- Select riders covering your most common risks.

- Consider the price hike versus the added safety you get.

- Ensure the total cost fits your yearly budget.

- Check IRDAI Guidelines for rules on rider expenses.

Which is better for you: riders or standalone policies?

Many people often ask: Is it better to get a rider or a separate policy? Rider life insurance can simplify things. You manage only one policy. Also, you typically pay just one premium. These riders often cost less than standalone policies. They provide good extra coverage. However, a rider's coverage amount is usually limited. It also ends when your main term policy stops.

What is the difference between a critical illness rider and a critical illness plan? Separate policies, like a critical illness plan from ICICI Lombard or HDFC ERGO, usually offer higher sum assured amounts. They give full coverage for specific health risks. A separate plan works on its own. Its duration does not rely on your term life policy. This gives you more choices and clear financial protection.

For those with high risks needing lots of specific coverage, a separate policy is often a better choice. Riders are great for adding protection if you have a budget. They suit people who need some extra coverage. Think about your risks and budget carefully. This helps you pick the right option for your needs.

Conclusion

Term insurance riders are useful tools. They help make your financial safety net stronger and fit your needs. Knowing each choice gives you better protection. A good rider life insurance add-on brings specific benefits to the policyholder. For example, a Waiver of Premium Rider can protect your policy. It helps even if you lose income due to a disability.

Choosing the right riders often depends on your unique situation. Think carefully about your health, money goals, and lifestyle. This ensures you build a strong plan that meets your exact needs. Do not just pick riders without thinking.

Use this guide to check your specific needs. Then, compare different term insurance plans. Look for insurers like HDFC Life or ICICI Lombard that offer the rider options you require. Make a smart choice for your family's future safety.

Frequently Asked Questions

Q: What is a term rider on a life insurance policy?

A term rider is an optional add-on that provides extra coverage, typically for specific risks like accidental death or critical illness, beyond your base policy. You'll pay a small additional premium for this enhanced protection. It applies for a defined period, separate from your main policy term (check IRDAI guidelines). This allows full coverage under one plan.

Q: Who is the rider in term insurance?

A rider in term insurance isn't a person at all; it's an optional add-on benefit you select. These typically enhance your basic policy, offering extra protection for things like critical illness or accidental death (this can vary). You just pay a small additional premium, but it's really useful for customizing your coverage.

Q: What is a 20 year term rider?

A 20-year term rider provides additional life cover for exactly two decades, added to your main insurance policy. If something unfortunate happens within those 20 years, your nominee receives an extra sum insured on top of your base policy benefits. It's a cost-effective way to boost protection for a specific period (this can vary slightly by insurer). This rider typically gives your family peace of mind during your peak earning years.

Q: Can I add a rider to my term policy after I have already purchased it?

No, you typically can't add a rider to your term policy once it's already purchased. Indian insurers usually require all riders to be selected at the time of policy issuance (this isn't generally allowed). Any new benefit typically demands a fresh underwriting assessment, which simply isn't feasible on an existing policy as per IRDAI guidelines.

Q: How does making a claim on a rider, like for a critical illness, affect my base policy's sum assured?

It really depends on whether your critical illness rider is 'accelerated' or 'additional'. Typically, an accelerated rider means a claim payout will reduce your base policy's sum assured by that amount. However, an additional rider doesn't affect the main sum assured, leaving it fully intact for your nominees (check your policy document for specifics).

Q: Is there a limit to the number of riders I can add to a single term insurance policy?

No, there isn't an IRDAI-mandated limit on the number of riders you can add. Each Indian insurer typically has its own internal guidelines for how many you can add (the total rider premium usually won't exceed your base premium). It's always best to check with your specific company; over-bundling them isn't always cost-effective.

Q: Does the coverage term for a rider have to be the same as the base policy's term?

No, a rider's coverage term typically cannot exceed the base policy's term. In fact, it's often concurrent, or in many cases, even shorter (depending on the specific rider type). Some insurers might cap rider terms, say at 20 years, even if your main policy runs longer; you'll need to confirm the policy document.

Q: Are the premiums paid for term insurance riders eligible for tax benefits?

Premiums for most term insurance riders typically qualify for tax benefits. You'll usually find them falling under Section 80C, sometimes Section 80D for health-related riders like Critical Illness (depending on the specific plan). The combined deduction for life insurance premiums, including these riders, is capped at Rs. 1.5 lakh in a financial year. Always confirm the exact eligibility with your insurer.